Oatly (OTLY) & Adobe (ADBE) - Earnings Breakdown

Oatly (OTLY) & Adobe (ADBE) - Earnings Breakdown

... a dive into their earnings reports

Together with… The Rollup

Outperform the crowd by following the pros 🤙 Curious what professional investors are doing with their money? The Rollup gives you the SparkNotes summary of the week's best investing content so you can quickly find out how the pros are allocating their capital.

Investors,

Welcome to the new version of our newsletter! We are excited to announce that we have revamped our content to bring you a fresh perspective on the world of business and finance. We understand that company earnings reports can be dry and complex, and not everyone is interested in analyzing them. That's why we've decided to broaden our focus and cover a wider range of topics that are relevant and engaging to our readers. We aim to provide you with insights and stories that are both informative and entertaining. We hope you enjoy our new approach and look forward to sharing more exciting content with you in the future.

Today we’ll be looking at Oatly (OTLY) and Adobe’s (ADBE) most recent earnings reports. So let’s get started.

Oatly (OTLY)

Oatly's share price has decreased by 90% since 2021: Oatly, the popular Swedish oat milk brand, has seen a significant decline in its share price since its initial public offering (IPO) in May 2021. The sharp drop in share price has raised concerns among investors and analysts regarding the company's long-term growth prospects and ability to deliver value to its shareholders.

The company's net income is continuing to decrease and is now in negative territory: Despite the company's claims of expanding market share, Oatly's net income has been contracting further into negative territory. This means that the company's expenses are higher than its revenue, resulting in losses.

The following chart is from their most recent earnings presentation.

Despite the negative financial indicators, Oatly has maintained that it is expanding its market share in the plant-based milk industry. The company's success in penetrating new markets, such as China, has been cited as evidence of this expansion.

Oatly's revenue per share has remained constant over the last few years and the company's EPS, which is the company's bottom-line profitability, has further decreased each quarter. This is a worrying trend as it suggests that the company is not generating sufficient profits to sustain its operations and investments.

Adobe (ADBE)

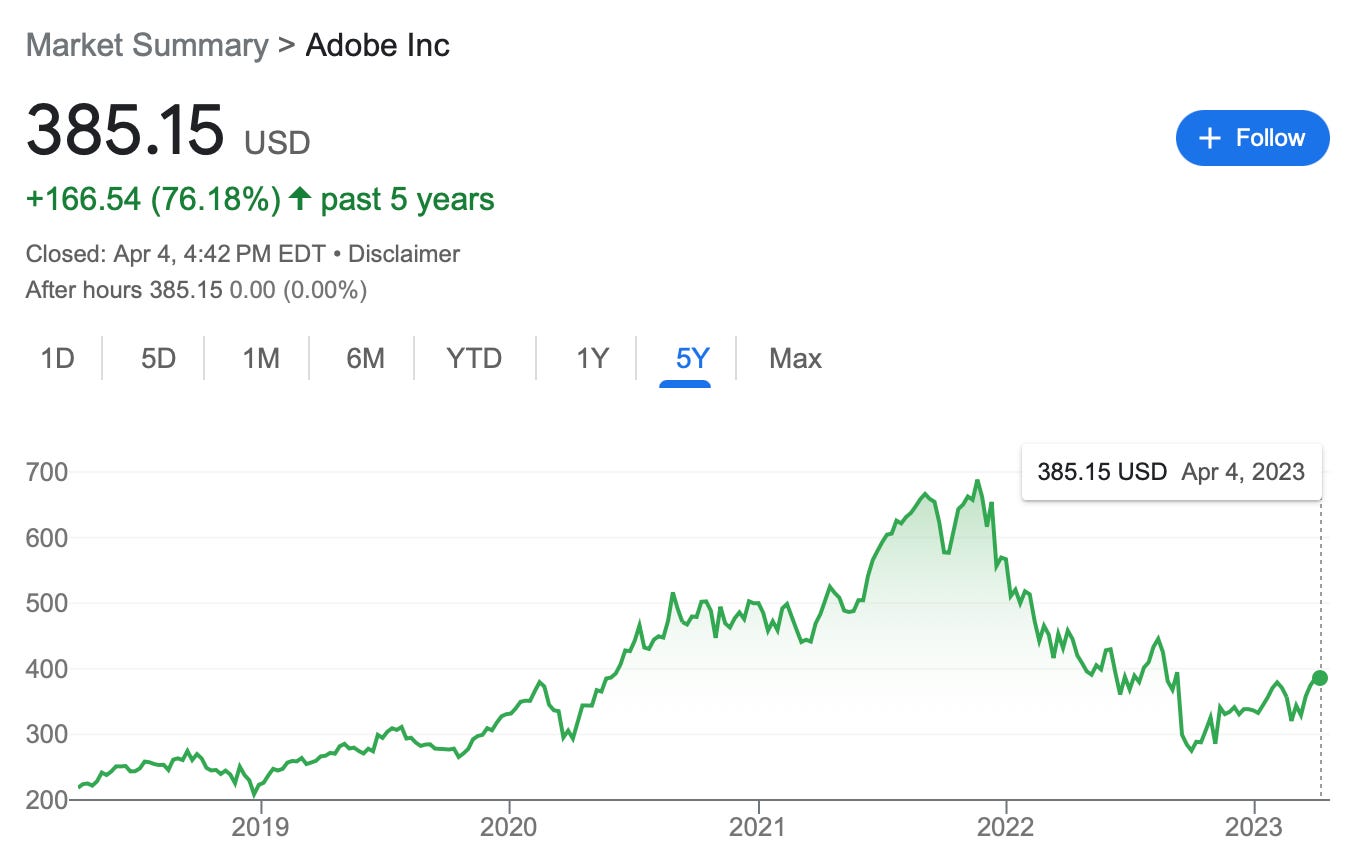

Adobe's share price is down 45% from the pandemic peak, but has held relatively strong compared to the broader market over the last year, -15% vs SPY -10%. The company's resilience during the pandemic is attributed to it’s diverse revenue streams and high customer loyalty.

Adobe's primary revenue source is digital media, which includes creative software products such as Photoshop and Illustrator. The company's dominance in the digital media industry has enabled it to maintain its leading position and generate substantial profits.

Adobe's impressive financial metrics demonstrate its ability to generate significant cash flows and profits. The company's high gross margins indicate that it has been able to price its products competitively while maintaining a healthy profit margin. Gross margins have remained constant at ~88% of revenue.

Adobe has been experiencing steady revenue growth of 12% year-over-year. The company's growth is attributed to its expanding customer base, product innovations, and successful marketing campaigns. The consistent revenue growth is a positive indicator of the company's long-term prospects.

From their recent earnings call, management noted:

“In Q1, we entered into a $1.4 billion share repurchase agreement, and we currently have $5.2 billion remaining of our $15 billion authorization granted in December 2020, which goes through the end of fiscal 2024.”

Hope you enjoyed today’s edition of the AlphaMemo, join us again next time for more earnings takes like these.

Disclaimer: All material presented in this newsletter is not to be regarded as investment advice, but for general informational purposes only. You are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, its moderators, and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer.