Lululemon (LULU) - How they make money?

... a dive into their earnings reports.

Together with… The Rollup

Outperform the crowd by following the pros 🤙 Curious what professional investors are doing with their money? The Rollup gives you the SparkNotes summary of the week's best investing content so you can quickly find out how the pros are allocating their capital.

Investors,

Earnings SZN is coming up and we’ll be diving into most popular company’s financials and where they saw growth. Think of it like your earnings season summary, but visualized.

Today we’ll be looking at Lululemon’s most recent quarter’s financials and earnings call. Let’s get started.

There’s a reason why LULU has out-performed the market by such margin over the last 5 years (or nearly any time period, really). Here’s the 5-year chart to get a visual on the returns.

I remember several years ago when the doubters and nay-sayers were perpetually touting that LULU was “over-priced” athletic-wear and their business model was not sustainable versus other, less-expensive, brands. So how does LULU make money?

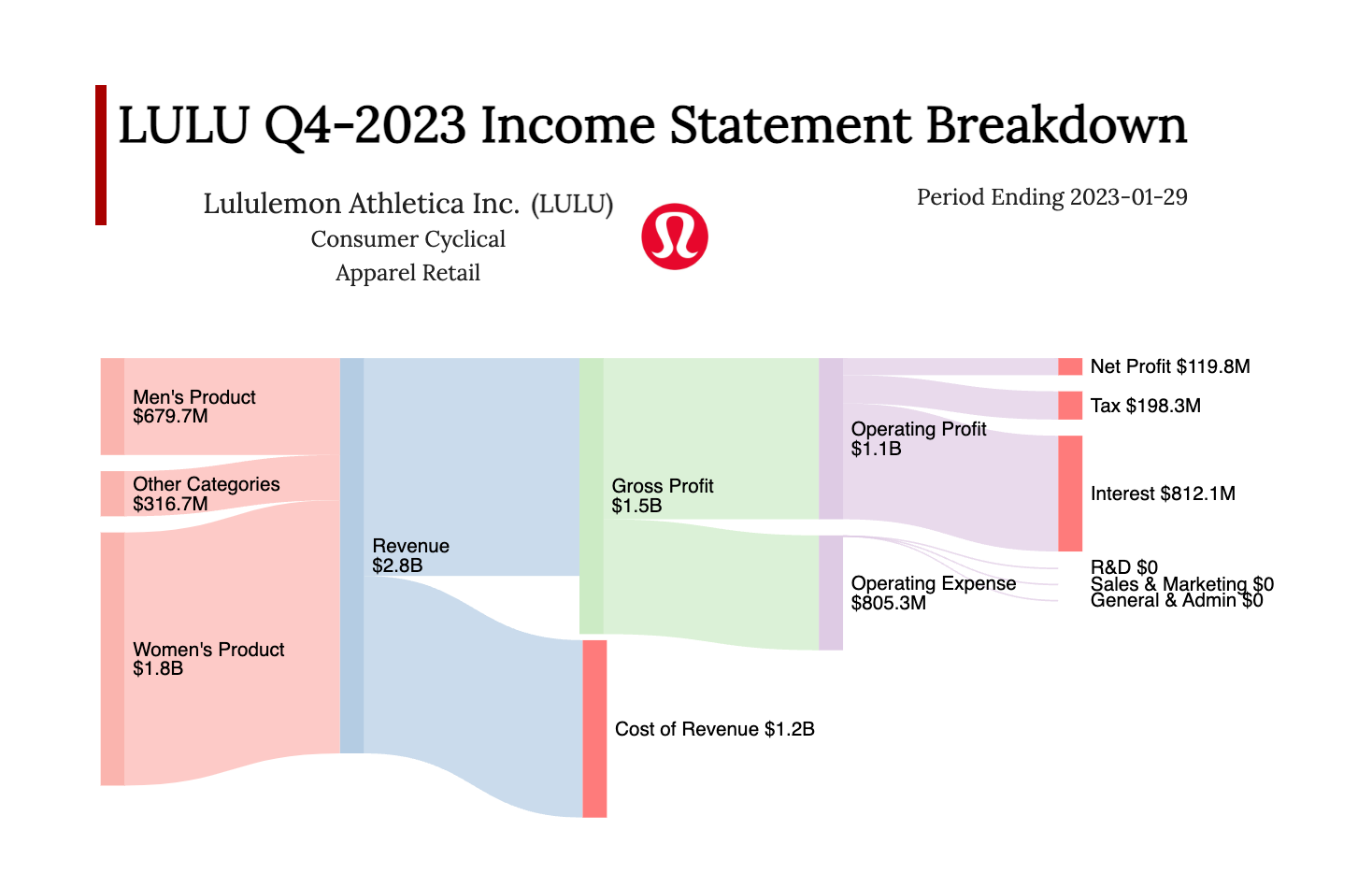

Here’s their most recent income statement, broken down:

Men’s product generates ~25% of revenues while women’s remains steady at 64%.

Their men’s line has grown 20% YoY for the same quarter, whereas women’s line grew 28%.

Gross margins of 55%.

From the earnings call…

Women's was up 23%. Our men's business was up 26%. And accessories was up 44%. We saw a 10% increase in company-operated stores and our e-commerce grew 46%. And by region, North America grew 24% and international increased 39%.

For a more detailed look here’s the same breakdown for each of the last 12 quarters.

While percentage of revenues seems to be relatively stable for each segment (men’s vs women’s) they have been growing consistently each quarter showing us that Lulu’s brand loyalty and product innovation remains very high on both sides.

Here’s one chart that really blows me away, it’s their Q4 revenue (most recent and holiday quarter) over the last 12 years. This thing is a monster as the company continues it’s accelerated growth on both top line and bottom-lines. LULU added $700 million in revenue from the same quarter just one year ago.

Although cash flows from their core product (athletic wear) has been extremely successful, their investment in MIRROR (think Peloton, but for Yoga/Pilates) has been somewhat underwhelming. Here’s what management had to say about it:

While members love our content, hardware sales did not match our expectations. And even though our CAC has continued to improve, it has not improved enough to maintain the current level of investment...

...On MIRROR, I just want to clarify, we're not eliminating the hardware, but we are adding an app feature that will allow a guest to sign up and pay a lower monthly subscription fee and acts the same content without having to purchase the hardware.

IMO management are very aware with what currently works, what doesn’t, and where to pivot. This is likely why the company has seen so much success and returned much of that value to shareholders that have believed in their process.

That’s all for today’s breakdown. Stay tuned for more just like this as we roll through earnings season.

Disclaimer: All material presented in this newsletter is not to be regarded as investment advice, but for general informational purposes only. You are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, its moderators, and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer.