ContextLogic (WISH - Full Stock Analysis): The Shopping Mall in your Pocket

This is a “Full Company Research” that was made public (free). Enjoy! To continue receiving posts like these, become a paying subscriber or subscribe to the free version that provides summaries only, below.

Overview

WISH controls the most popular shopping mobile application in the world. In short, the company is a direct-to-consumer online retailer. However, a few key features differentiate it from its competition:

WISH does not operate any brick-and-mortar locations

WISH does not target popular branded items in its offerings

WISH oftentimes works directly with the manufacturers or independent sellers instead of the wholesaler

Let’s go through this list to understand why this is a significant differentiation.

WISH not operating any brick-and-mortar locations allows it to maintain low capital expenditures (CAPEX) and frees up its cash flows.

WISH’s focus on unbranded items allows it to compete in a more niche market that has not been taken over by other e-commerce giants. This is a space that WISH dominates.

WISH’s decision to work directly with manufacturers rather than wholesalers allows it to procure its product catalog at a much cheaper price point than any competitor which it then passes on to its customers. With independent sellers, WISH offers a more unique product catalog than its competitors.

These three features combined defines how it interacts with its customer base. WISH targets mostly younger, low to middle income households. It offers cheap and unbranded products, an area that was historically ignored by larger e-commerce companies. Even their strategy to be a mobile app reflects this. According to Pew Research, lower-income shoppers accessed the internet solely through their smartphone at a rate double the other income brackets (source).

The Future of E-commerce is Mobile

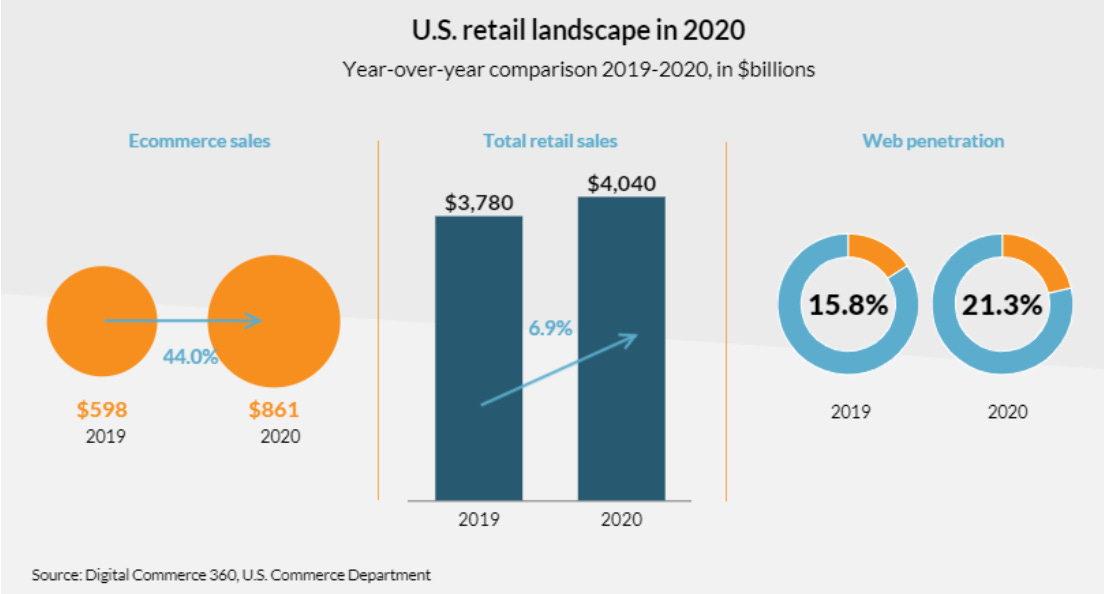

E-commerce is not a new term. Years ago, a CEO at Sears might have argued that people prefer an in-store experience. Today, that same CEO would finally admit that he was incorrect in underestimating the prominence of e-commerce. However, what most people do not know is that e-commerce is still in its growth phase. Although due to COVID, 2021 represented one of the highest growth years ever for e-commerce (source). Its growth in Q1 2020 over tripled the growth in Q3 and Q4 of 2019. In 2020, online spending represented 21% of the total retail sales while in 2019, online spending represented only 16% (source).

Furthermore, the growth is mostly being captured by the American and European markets (source). This is especially useful for WISH as over 80% of its global sales is coming from these two regions (source).

A few macro trends are expected to drive e-commerce for the next decade:

Mobile shopping: COVID-19 accelerated the shift to online shopping by over 5 years (source)! Mobile commerce or m-commerce is expected to continue breaking out over the next few years, rising at a rate of 25.5% compounded annual growth rate. Its expected that by 2024, m-commerce will represent 44% of all e-commerce transactions accounting for ~$500B in sales (source).

Big data and AI: A key advantage in e-commerce is going to be in data whether that is to power a recommendation feature or to power targeted advertisements, data is the new gold for e-commerce companies. Increasingly, the ability to personalize the shopping experience per user is becoming a crucial differentiator. BCG reports that proper personalization can increase sales by over 25% (source).

WISH, More than Just a Retailer

WISH has a few main product lines:

Online retail store, the Wish mobile application

ProductBoost, a marketing service on the Wish mobile application

WishLocal, a digital presence service for smaller brick-and-mortar retailers

Wish Express, a logistics service for customer delivery

1. WISH as an online retail store

As an online retail store, WISH is growing quickly in all areas. As of 2021, its revenue per active user increased 76% YOY, led by an increase in orders over $20 which increased over 50% in Q1 2021. However, total monthly active users declined 7% YOY which may indicate some saturation in their market (source).

As stated before, the key differentiator in the future of online retail is going to be personalization through big data and AI. WISH is uniquely positioned to capture this core advantage. At its very inception, WISH has always recognized the value of data. As of 2020, WISH catalogued the following data points (source):

100M+ monthly active users: their age, gender, location, etc.

150M+ activities on Wish: clicks, scrolls, items sold, etc.

500K+ merchant data: refund rates, ship times, etc.

640M+ items shipped: ratings, pictures, etc.

Through this enormous warehouse of data, WISH was able to build one of the most effective recommendation engines in the world. WISH sees 70% of their sales coming from purchases not involved with a search query (source). This speaks volume on the effectiveness of their data science platform and their ability to understand their customer, which in turn enables…

2. ProductBoost, the AdWords for Shopping

By proving out a deep knowledge of their customer base, WISH can show relevant targeted ads to its user-base. In 2020, 30% of all merchants on WISH used this service to increase their sales which represented $140M of revenue for WISH (source). The company is very focused in growing this area as it represents a scalable, high-margin service offering for them. As of Q1 of 2021, they are already seeing a 14% increase in sales in this area compared to Q4 of 2019 (source).

3. WishLocal, Helping those Behind the Curve

WishLocal is a service that brick-and-mortar retailers sign up for. Through WishLocal, they agree to become a drop point for WISH products in return for a fee. They will both earn the fee as well as can cross-sell to the customer. This also serves as an incentive point for them to sign onto Wish as a merchant. While WishLocal is not a revenue generating feature, it is a point of differentiation that allows Wish to have a physical presence without the need for heavy investment in brick-and-mortar stores.

4. Wish Express, Driving Business Forward

Wish Express is the global logistics service at WISH. They contract out other delivery services from local vendors and stitch it all together into a single product. Like this, they can both improve their own delivery services (shipping-related refunds were down 40+% in 2021) as well as to offer another revenue generating service to their merchants and partners. In 2021, their logistics revenue was ~$250M which represented a 338% increase from the previous year (source).

Strong Balance Sheet, Weak Income Statement

WISH is a risky company, and this is reflected in their finances. They have a cash reserve of $2B which is balanced out with nearly $900M in current liabilities. In 2020, they issued $1B in new stock whose funds were used to absorb a $750M net operating loss. This represents a major risk for the company as an operating loss of this magnitude will not be sustainable for more than 2 years.

The $750M operating loss was mostly made up of an extremely high marketing expense and a reduction in their gross margins (source). The SG&A (primarily driven by marketing) expense went up by 40% which corresponds to a 33% increase in sales indicating an inefficient usage of resources.

While the marketing expense can be easily controlled, it’s a little worrisome to see their gross margins reduced from 80% in 2019 to 64% in 2020 especially as they have a long-term goal of 75% margins (source). If WISH cannot get their margins back and maintains current levels of spending, another share dilution will be necessary next year as well to sustain its balance sheet health.

In 2020 WISH did 2.54 billion in revenue, a 33.7% increase from 2019 revenues. Their trailing twelve month (TTM) gross margin is roughly 60%, which is very good for the e-commerce industry where it is usually closer to the 40% range. Like mentioned above, WISH's SG&A expense is absolutely huge and one of the main factors of why they are burning through cash.

In their most recent earnings report, WISH management guided revenues of 715-730 million revenue for Q2 2021. What’s concerning is that it’s only 2-4% growth when looking YoY (source), however, management noted that this is mainly due to the incredible growth they experience the year prior as lockdowns became normalized around the world. This ties back to the debate of whether or not their target market is seeing saturation.

The Bottom Line

In many ways, WISH reminds me of an early Amazon. Perhaps their story will end similarly to Amazon as well where they become a global tech giant valued well past where they were as an online retail store. After all, they have many things going for them:

The most downloaded shopping app in the world

High market share in the niche unbranded sales space

Expansion into high margin services

However, there are some warning signs to recognize as to how WISH may not be the next Amazon.

Amazon already exists and it competes against WISH

It lost monthly active users in the year it spent the most in marketing

Its gross margins declined in 2020 (though its been steadily rising beforehand)

For me, I see a company with $1B of extra cash above its current liabilities and revenues of $2B being valued at $8.5B. I believe the $8.5B valuation reflects the risk that WISH incurs burning through $750M of cash in a year (it only happened once, 2019 was much better). If WISH can figure out a way to stem the bleeding of cash or to raise funds without a share dilution, their stock price should rise as a result.

With their focus on data, their considerable market share, and some core high margin products already underway, I believe that WISH is poised for growth in 2021.

TLDR;

WISH is in the e-commerce space and they are what I would call a "flea market in your pocket" that gives you access to thousands of products directly from their mobile app. They do not operate brick and mortar locations, and they do not target branded items which allows them to work directly with manufacturers instead of wholesalers (cutting out the middle man and saving on expenses).

WISH is able to dominate this very niche space because the big e-commerce players simply do not care about selling discount items of this type. WISH's customer-base is targeted toward the low-to-middle class which is evident if you go to their site. Many products are under $5 and in unusual categories to say the least.

One advantage in WISH's business model is the fact that they create a bridge between the customer and the manufacturer, cutting out the middle-man while maintaining low capital expenditures (CapEx), which free's up their cash flow to spend on things like customer acquisition.

When it comes to their fundamentals WISH is a "risky" company. They aren't overly indebted, but still hold roughly 900m liabilities compared to their 2B cash reserve. Most of their expenses are marketing expenses and they burn through a significant amount of money on customer acquisition. This might present the risk of new share issuance and dilution should the stock price out-perform in a short period of time.

Having said all that, their gross margin (~60%) is quite healthy. For a company that trades at only 3x sales they have the potential to out-perform the market should they figure out a way to retain customers without spending billions on SG&A expenses. In short, they are doing just under 3 billion in sales and have a market cap of 8.7 billion dollars.

If you liked the post, why not share it?

Positions Disclosure: It can be assumed the author of this article has a long position in the stock.

Disclaimer: All material presented in this newsletter is not to be regarded as investment advice, but for general informational purposes only. You are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, its moderators, and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer.

i WISH to the moon

I'd like to see what I paid for $$"